An FHA loan is a mortgage loan that’s backed by the Federal Housing Administration. Borrowers are required to pay a mortgage insurance premium, which reduces the lender’s risk if a borrower defaults.FHA loans are available to all types of borrowers, not just first-time homebuyers.

The program is available for both purchase and refinance mortgages. There are some restrictions on FHA loans, such as maximum loan limits, but these vary by county.

An FHA loan is a mortgage loan that is insured by the Federal Housing Administration (FHA). These loans are available to homebuyers with low credit scores or limited funds for a down payment.The FHA insures these loans, which means that if the borrower defaults on the loan, the lender will be reimbursed by the FHA.

This makes these loans less risky for lenders and more accessible to borrowers who may not qualify for a conventional mortgage.There are some drawbacks to FHA loans, however. They generally have higher interest rates than conventional mortgages and require borrowers to pay for private mortgage insurance (PMI) if they do not put down at least 20% of the purchase price upfront.

If you are considering an FHA loan, it is important to compare offers from multiple lenders to ensure you are getting the best deal possible.

What is a FHA Loan & How Does It Work?

What is a Fha Loan And How Does It Work?

A FHA loan is a mortgage that’s insured by the Federal Housing Administration (FHA). They are popular especially among first time home buyers because they allow down payments of 3.5% for credit scores of 580+. However, borrowers must pay mortgage insurance premiums, which protects the lender if a borrower defaults on their mortgage.

How do FHA loans work?The Federal Housing Administration (FHA) doesn’t actually lend money to homebuyers. Instead, it insures mortgages, making it less risky for lenders to offer loans with low down payments and more flexible terms.

That way, more people can qualify for homeownership even if they don’t have 20% to put down or a perfect credit score.To get an FHA loan, find a bank that offers them and fill out an application. The lender will then have the house appraised to make sure it’s worth at least as much as the loan amount you’re requesting.

If everything checks out, you’ll be approved for the loan and can start shopping for a home! Just remember that you’ll have to pay both your monthly mortgage payments and your FHA insurance premiums every month.

What is the Purpose of an Fha Loan?

An FHA loan is a mortgage loan that’s backed by the Federal Housing Administration. Borrowers are required to pay a mortgage insurance premium, which reduces the lender’s risk if a borrower defaults.The FHA doesn’t actually make home loans.

It insures them for lenders. If a borrower defaults on an FHA-backed loan, the lender can file a claim for reimbursement with the government. That way, borrowers who might not otherwise qualify for a conventional mortgage have access to financing.

FHA loans are available for both purchase and refinance transactions. In order to be eligible, borrowers must have steady employment history, good credit, and reasonable debt-to-income ratios. They also must occupy the property as their primary residence and be US citizens or legal permanent residents.

What is the Difference between Fha And a Regular Loan?

There are several differences between FHA loans and regular, or conventional, mortgages. Perhaps the most notable difference is that FHA loans require both an upfront mortgage insurance premium (UFMIP) and a monthly mortgage insurance premium (MIP), while conventional loans only require private mortgage insurance (PMI) if you make less than a 20% down payment.Other differences include:

-FHA loan limits are lower than conventional loan limits in most areas

-FHA loans may be assumable by another qualified borrower, while most conventional loans are not assumable

Credit: www.newamericanfunding.com

What is a Fha Loan And Who Qualifies?

If you’re looking to purchase a home, you may be wondering if a FHA loan is right for you. FHA loans are mortgages that are insured by the Federal Housing Administration, and they are available to both first-time homebuyers and repeat buyers. In this post, we’ll discuss what a FHA loan is, who qualifies for one, and how to apply.

What is an FHA Loan?An FHA loan is a mortgage that is insured by the Federal Housing Administration. The main benefit of an FHA loan is that it allows borrowers to put down as little as 3.5% for a down payment, which can make purchasing a home more accessible for those who don’t have the savings for a conventional down payment.

Another benefit of an FHA loan is that it has more flexible credit requirements than a conventional mortgage, making it easier for those with limited credit history to qualify. Lastly, if you do default on your FHA loan, the government will cover some or all of the loss to the lender, which provides additional protection.Who Qualifies For An Fha Loan?

In order to qualify for an FHA loan, borrowers must have at least two established lines of credit and a debt-to-income ratio of 50% or less. Additionally, applicants must have steady employment history and demonstrate an ability to afford monthly mortgage payments. As mentioned above, those with limited credit history may still qualify for an FHA loan if they can meet these other criteria.

How Do I Apply For AnFha Loan?Applying for anFha Loanisn’t much different from applyingfor any other typeofmortgage . You’ll work with alenderto complete acredit application , provide documentationof your employmentand financial situation , and go through underwriting .

Once approved , you’ll work with your lender topay closing costsand finalizeloan details prior toyour closing date .

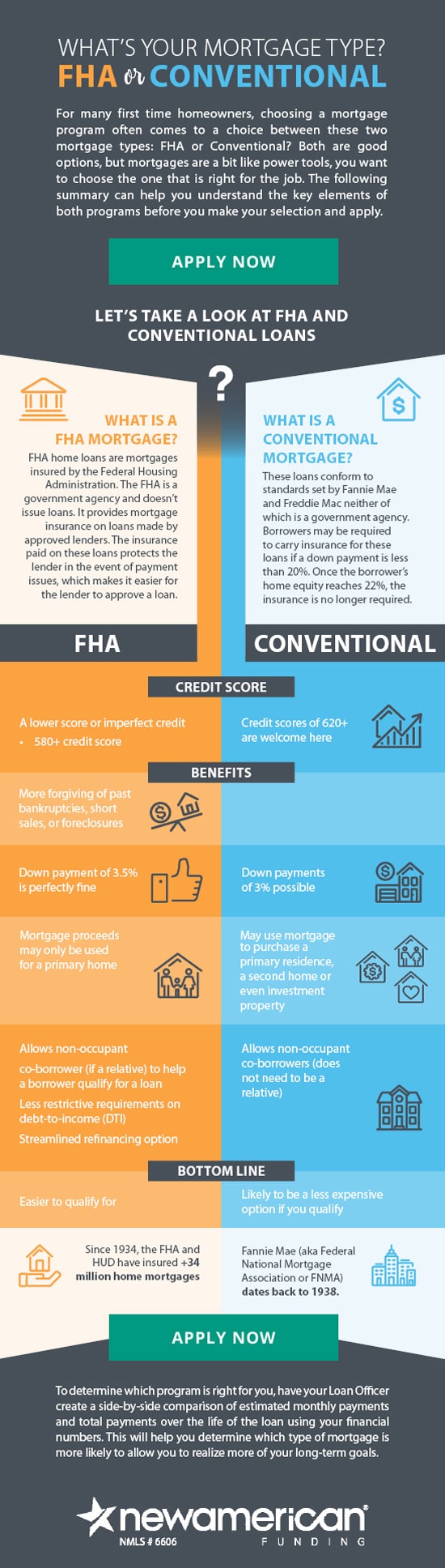

Fha Loan Vs Conventional

When it comes to financing your home, there are many different options available. Two of the most popular options are FHA loans and conventional loans. So, which one is right for you?

Here’s a quick rundown of each loan program and how they differ:FHA Loans:FHA loans are government-backed loans that are available to all qualifying borrowers.

They require a minimum down payment of 3.5% and have more relaxed credit requirements than conventional loans. Additionally, FHA loans come with lower interest rates and monthly mortgage insurance premiums (MIP). However, one downside to FHA loans is that they require the borrower to pay an upfront MIP fee, which can be quite costly.

Conventional Loans:Conventional loans are not backed by the government and can be obtained through private lenders. These loans usually require a higher credit score than FHA loans and often come with stricter underwriting guidelines.

In terms of down payments, conventional loan programs can vary greatly – some as low as 3%, while others may require up to 20% down depending on the lender’s guidelines. Interest rates on conventional loans also tend to be higher than those on FHA loans but overall monthly payments will be lower if you opt for a shorter loan term (15 years vs 30 years).

Fha Loan Calculator

An FHA loan calculator is a great tool to use when you are considering an FHA loan. It can help you determine if you will qualify for the loan, how much you can afford to borrow, and what your monthly payments will be. The FHA loan calculator is easy to use and can give you peace of mind when shopping for a home.

What is Fha

FHA is the Federal Housing Administration, a US government agency that provides mortgage insurance on home loans made by FHA-approved lenders. The insurance protects the lender against loss if the borrower defaults on the loan.FHA was established in 1934 as part of the National Housing Act.

Its original purpose was to help make home ownership more affordable for American families by providing mortgage insurance on home loans with low down payments.Over time, FHA has evolved into a program that not only helps first-time home buyers with low down payments, but also supports homeownership for people with less than perfect credit histories. Today, FHA insures mortgages on single family homes, manufactured homes, and condominiums.

It also insures reverse mortgages (HECMs) and assists homeowners who are struggling to make their mortgage payments (through its Home Affordable Modification Program).If you’re thinking about buying a home, it’s worth taking the time to learn about how FHA can help you finance your purchase.

Fha Loan Requirements 2022

If you’re looking to get an FHA loan in 2022, you’ll need to meet a few requirements. For starters, you’ll need a credit score of at least 580. You’ll also need to have a down payment of at least 3.5%.

And finally, you’ll need to have a debt-to-income ratio that’s no more than 43%. If you can meet these requirements, then you should be able to qualify for an FHA loan.

Fha Loan Income Requirements

There are many different types of FHA loans available to borrowers, and each has its own set of income requirements. In order to qualify for an FHA loan, borrowers must have a steady source of income that can be verified by the lender. This can come in the form of wages from employment, self-employment, alimony payments, child support payments, or other regular sources of income.

In general, lenders will require that borrowers have a debt-to-income ratio of no more than 43% in order to qualify for an FHA loan. This means that your total monthly debts (including your mortgage payment) should not exceed 43% of your gross monthly income. However, there are some exceptions to this rule and certain borrowers may be able to qualify with a higher debt-to-income ratio.

If you’re self-employed or earn income from sources other than traditional employment, you may still be able to qualify for an FHA loan. Lenders will typically require that you have a two-year history of consistent earnings in order to qualify. Additionally, they may require additional documentation such as tax returns or bank statements in order to verify your income.

If you’re looking to get an FHA loan but don’t think you meet the usual income requirements, there may still be options available to you. Talk to a qualified lender about your specific situation and see what kind of options they can offer you.

Fha Loan Application

FHA loans are a popular choice for first-time homebuyers and those with limited credit history or income. An FHA loan is a mortgage that’s insured by the Federal Housing Administration (FHA). This type of loan requires as little as 3.5% for a down payment, making it a great option for first-time homebuyers.

If you’re looking to apply for an FHA loan, you’ll need to gather some essential information first. This includes proof of employment and income, your Social Security number, and details about your monthly housing costs. You can find more information on the FHA website or speak to a lender about getting started with your application.

Fha Loan Pre Approval

If you’re looking to get pre-approved for an FHA loan, you’ll need to provide the lender with a variety of information. This includes your social security number, income and employment information, as well as your bank account details. The lender will then pull your credit report and evaluate your financial history to determine if you’re eligible for an FHA loan.

If you are, they’ll provide you with a pre-approval letter that you can use when shopping for a home.There are a few things to keep in mind when getting pre-approved for an FHA loan. First, the process is not instantaneous – it can take several days or even weeks for the lender to review your information and make a decision.

Second, being pre-approved does not guarantee that you will ultimately be approved for the loan – if your financial situation changes during the application process, the lender may reconsider their decision. Finally, remember that getting pre-approved is just one step in the homebuying process – you’ll still need to find a property that meets all of the requirements of the FHA program before you can close on your loan.

Conclusion

An FHA loan is a mortgage that’s insured by the Federal Housing Administration (FHA). They are popular especially among first time home buyers because they allow down payments of 3.5% for credit scores of 580+. However, borrowers must pay mortgage insurance premiums, which protects the lender if a borrower defaults on their loan.